Omics Solution Provider Market Map

We present the first comprehensive map of the Omics Solution Provider landscape.

You either die a solution provider or you live long enough to see yourself become a drug discovery company. Or do you?...

As biology advances exponentially, new multi-omic technologies to read, write, and edit cells (genome, proteome, metabolome, or epigenome) emerge every week, rapidly increasing the level of complexity. Techniques that would have made the cover of Nature Biotech ten years ago are now standard in experimental protocols. Skills that once required an entire PhD and postdoc to master are now routinely expected from a first-year research associate.

How are we supposed to keep exploring the farthest boundaries of biological possibilities if even the most basic discoveries depend on such complex and rapidly changing multi-omic technologies?

Enter biological solutions providers. They play a crucial role in transforming cutting-edge biology into accessible solutions by abstracting these complex but essential tools into services, kits, or instruments.

Within Omics, solution providers usually focus on genomics, proteomics, multi-omics, single-cell, or spatial biology.

Whether it's a $100 whole genome sequencing, a detailed mapping of the spatial epigenome at single-cell resolution, the sequencing of a million cells simultaneously, or high-throughput cloning of plasmids into bacteria—impossible feats a decade ago—can now be accomplished in just a few hours with the help of Ultima Genomics, AtlasXomics, Fluent Biosciences, or Seqwell, respectively.

We wanted to break down the Omics Solution Provider space into a digestible format that anyone can understand. Through numerous conversations with researchers, scientists, academics, and customers, we sought to create a market map.

Going into this, we understood that any categories we grouped them into would be reductionist. Some companies fit well into multiple categories, and others don’t fit well into any of them. We did our best to balance usability and accuracy.

We also looked into the dataset (DM and I’ll share) and found some interesting insights. Here are a few of them:

1) Company inceptions peaked in 2016, with noticeable decreases around 2007-08 and 2022-23.

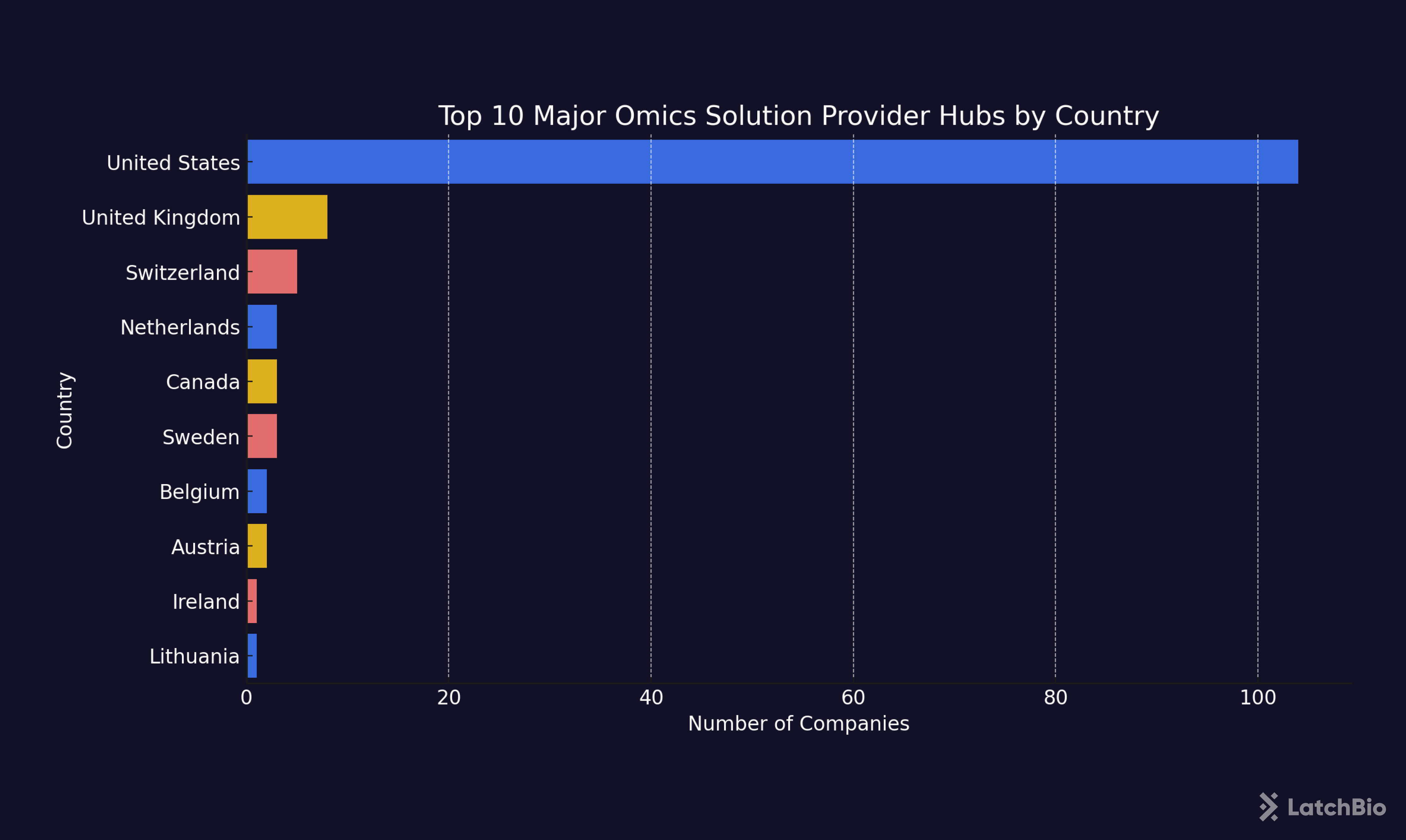

2) The major hubs are as expected:

For cities:

San Diego

Cambridge, Boston, San Jose (tie)

South San Francisco

For countries:

United States (by far)

United Kingdom

Switzerland

3) And the old age discussion: What if we divide by metropolitan area? Blessed be thy bay.

Bay Area

Boston Area

San Diego Area

4) Lastly, the majority of the companies in our dataset fall within the 11 to 50 employees range, pointing to an up-and-coming wave of new solution providers in the near and medium-term future.

That's it. This is obviously a work in progress, and we expect to rapidly update our dataset as we learn more about the space and as it keeps improving quickly.

As usual, if you are interested in this space, I would love to chat. Please DM me or reach out at alfredo (at) latch (dot) bio.

Thanks for sharing.

It's surprising not to see any Chinese companies represented here.